You might think an online home estimate is close enough to a real appraisal. Most buyers and sellers in Colorado make exactly that assumption, and it regularly costs them thousands of dollars at the closing table. A formal appraisal is an evidence-development process tied to specific reporting standards, not just a data algorithm pulling recent sales. This guide walks you through every stage of the appraisal process, explains the methods appraisers use, and shows you exactly what to do when things go sideways.

Table of Contents

- What is a real estate appraisal?

- How the appraisal process works in Colorado

- Appraisal methods: Sales comparison, cost, and income approaches

- What happens if your home appraises low?

- Why real estate appraisals matter more than you think

- How HomeSavvy Colorado makes appraisal and valuation easier

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Appraisals vs. estimates | A real estate appraisal is a formal process conducted by a licensed appraiser, unlike quick online value tools. |

| Colorado standards | Appraisals for loans in Colorado follow strict USPAP rules and state licensing requirements. |

| Appraisal methods | Appraisers use sales comparison, cost, or income approaches and must reconcile these methods for a final value. |

| Handling low appraisals | If an appraisal is low, options include renegotiation, extra cash, or contract contingencies. |

| Value in decisions | Understanding appraisals empowers buyers and sellers to make smarter, more confident choices. |

What is a real estate appraisal?

A real estate appraisal is a formal, unbiased opinion of property value prepared by a licensed professional for a specific purpose. That purpose matters enormously. An appraisal completed for a mortgage lender is not the same as one prepared for a divorce settlement or an estate. The intended use shapes the scope, the standards applied, and what the appraiser is actually required to report.

In Colorado, appraisals used for mortgage lending must be performed by appraisers who hold a state-issued license or certification. This is not optional. Colorado's appraiser licensing regime is tied directly to federal USPAP requirements, which stands for the Uniform Standards of Professional Appraisal Practice. Think of USPAP as the rulebook that every legitimate appraisal in the country must follow.

Here is what a real estate appraisal is and is not:

- Is: A formal value opinion backed by market data, physical inspection, and documented analysis

- Is: A legal document required by most mortgage lenders before funding a loan

- Is: Conducted by an independent, licensed professional with no financial stake in the outcome

- Is not: An automated estimate from a real estate website

- Is not: An agent's comparative market analysis, even when prepared carefully

- Is not: An assessment for property tax purposes (that comes from your county assessor)

Appraisers in Colorado apply up to three recognized valuation approaches to develop their opinion: the sales comparison approach, the cost approach, and the income approach. Which methods they use depends on your property type and the assignment's purpose, which we will cover in detail below.

"The appraisal report represents a professional standard, not a simple online estimate. Lenders, courts, and buyers rely on it precisely because it's built on verifiable evidence and follows a structured process."

Now that you know why appraisals are more than simple estimates, let's break down the process step by step.

How the appraisal process works in Colorado

A well-organized appraisal workflow follows a consistent sequence of stages, from defining the assignment all the way through delivering a compliant written report. Understanding each stage helps you prepare and avoid surprises.

Here is what happens from start to finish:

- Define the assignment. The appraiser clarifies the purpose (mortgage, refinance, estate, etc.), the property rights being valued, and the effective date of value. This sets the entire scope of work.

- Gather preliminary data. The appraiser pulls public records, tax data, prior sales history, and any relevant disclosures about the property.

- Conduct the physical inspection. The appraiser visits the home, measures square footage, notes condition, records upgrades and deferred maintenance, and photographs interior and exterior features.

- Research comparable sales. Also called "comps," these are recent, nearby sales of similar properties used as benchmarks for value.

- Apply valuation approaches. Depending on the property type, the appraiser runs one or more of the three standard methods and documents the analysis.

- Reconcile the value indications. When more than one approach is used, the appraiser weighs the results and explains which carries the most weight and why.

- Prepare and deliver the report. The final report is formatted to lender and USPAP standards and delivered to the client, usually the lender.

What to expect at each stage as a buyer or seller

During the inspection, plan for the appraiser to spend 30 to 60 minutes inside a typical single-family home. Larger properties or those with complex features take longer. Sellers should make sure the property is clean and accessible. Fix obvious maintenance issues beforehand, because a broken handrail or a missing smoke detector can affect condition ratings.

After the inspection, the process mostly happens behind the scenes. The appraiser analyzes data, adjusts comps, and writes the report. Buyers should expect the final report to arrive within three to seven business days of the inspection, though tight markets or rural Colorado properties can push that timeline longer.

Understanding the role of USPAP compliance

USPAP compliance is not bureaucratic red tape. It protects you. It means the appraiser cannot change their opinion because a lender pressures them, and it means the analysis must be transparent and documented. When making smart choices with property data, understanding how an appraisal was built is as important as knowing the final number.

| Stage | Who is involved | Typical timeline |

|---|---|---|

| Assignment definition | Appraiser, lender | Day 1 |

| Property inspection | Appraiser, homeowner/seller | Day 2 to 4 |

| Data analysis and comps | Appraiser | Day 3 to 6 |

| Report writing | Appraiser | Day 5 to 7 |

| Report delivery to lender | Appraiser, lender | Day 7 to 10 |

Pro Tip: Prepare a one-page summary of recent improvements you have made to the home, including the year of the upgrade and approximate cost. Hand it to the appraiser during the inspection. Appraisers are not required to accept it, but it puts relevant data directly in front of them at the right moment and can influence how they account for upgrades.

You can also use PropertyIQ for instant estimates before the formal appraisal is ordered to set your expectations about where the value might land.

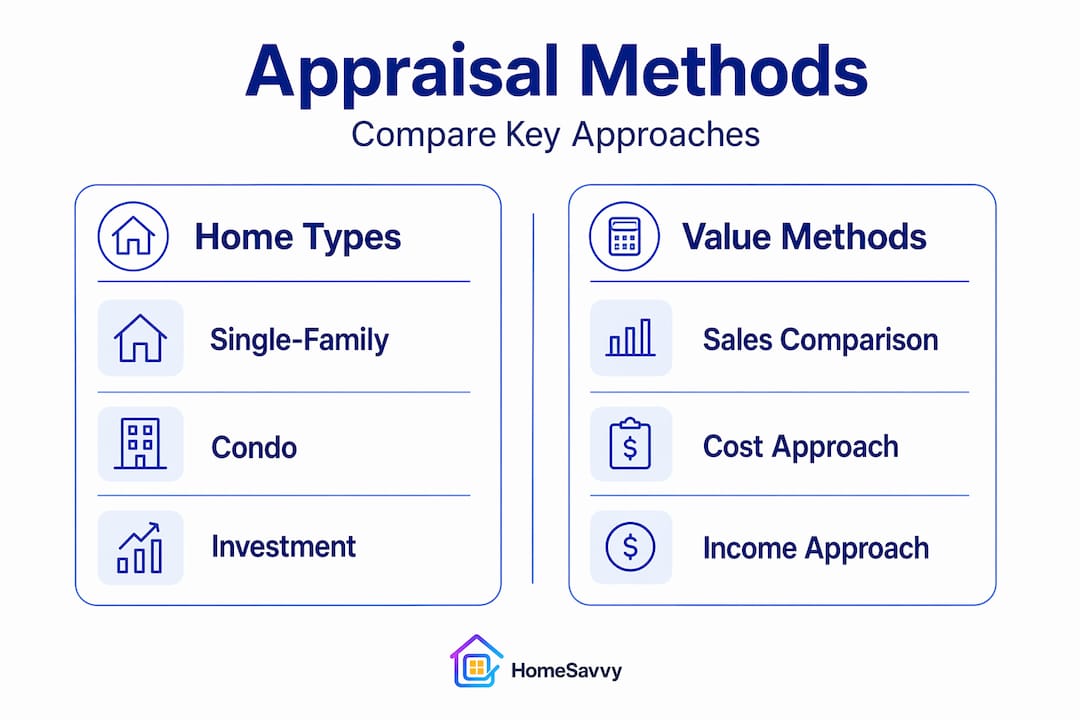

Appraisal methods: Sales comparison, cost, and income approaches

Knowing the steps, it's essential to understand the methods appraisers use to develop value opinions. Each approach asks a different question about the property, and each has strengths and limitations in the Colorado market.

Sales comparison approach

This is the most widely used method for residential properties. The appraiser finds three to six recently sold homes that are similar in size, condition, age, and location to the subject property. They then make dollar adjustments to account for differences. For example, if a comparable home had a three-car garage and yours has two, the appraiser subtracts an estimated value for that difference.

In active Colorado markets like Denver, Boulder, or Colorado Springs, there are usually enough sales to make this approach highly reliable. In rural areas or mountain communities, finding truly comparable sales can be difficult, which is why appraisers sometimes have to pull comps from a wider geographic area or an older time period.

Cost approach

The cost approach estimates value by calculating what it would cost to rebuild the home from scratch, adjusted for depreciation, and then adding the land value separately. This method is most relevant for new construction, unique properties that rarely sell, or special-use buildings where comparable sales simply do not exist.

In practice, for a standard 1990s suburban home in the Denver metro, the cost approach carries less weight because depreciation estimates involve significant judgment. For a brand-new custom build in a mountain resort area, it may be the primary method.

Income approach

The income approach converts rental income into a value estimate using capitalization rates or discounted cash flow analysis. This method is most relevant for investment properties, duplexes, small multifamily buildings, and any property where the primary value driver is its income-producing ability rather than its appeal to an owner-occupant.

Pro Tip: If you own a rental property in Colorado and are planning to refinance or sell, make sure your rent rolls, lease agreements, and vacancy history are organized and ready to share. Appraisers using the income approach will need this data to develop a credible value.

| Method | Best used for | Strength | Limitation |

|---|---|---|---|

| Sales comparison | Single-family homes, condos | Reflects actual market behavior | Requires adequate recent sales |

| Cost approach | New construction, unique homes | Useful when sales are scarce | Depreciation is subjective |

| Income approach | Rentals, multifamily properties | Captures income-driven value | Relies on reliable income data |

What happens if your home appraises low?

Now that we've covered the methods, let's address one of the most stressful moments in a deal. The appraisal comes back at $30,000 below the contract price. Your stomach drops. What do you actually do?

First, understand that this situation is more common than most people realize, especially when buyers are competing aggressively and contracts are written over list price. When a home appraises below contract price, Colorado buyers and sellers have several legitimate paths forward.

The three main resolution strategies:

- Renegotiate the price. The seller agrees to lower the contract price to the appraised value. This is the cleanest solution and the one buyers typically push for first.

- Buyer covers the gap. The buyer agrees to pay the difference between the appraised value and the contract price in cash. This is called an appraisal gap, and some buyers even build an "appraisal gap guarantee" clause into their original offer in competitive markets.

- Invoke the appraisal contingency. Colorado's standard purchase contract includes an appraisal contingency that lets buyers terminate the deal and recover their earnest money if the appraisal comes in low and parties cannot agree on a resolution.

How to position yourself before the appraisal happens

The best time to manage appraisal risk is before the appraiser shows up, not after. Understanding why appraisal outcomes matter starts with knowing what you paid, why you paid it, and whether data supports that price. If you are a seller, pricing your home accurately from the start reduces the chance of landing in an appraisal gap situation in the first place.

Buyers who use commission rebate strategies have more flexibility to cover small gaps without blowing up their budget. And having a detailed Colorado home sale checklist in place ensures both sides of a transaction have addressed every potential issue before the appraisal becomes a problem.

Pro Tip: Document every negotiation in writing. If you and the seller agree to lower the price or split the gap, get it in a signed amendment immediately. Verbal agreements mean nothing once closing day pressure sets in.

A note on reconsideration of value

If you believe the appraisal contains factual errors, like wrong square footage, missed comparable sales, or incorrect adjustment amounts, you can request a reconsideration of value. This is a formal process, not just a complaint. You need to provide specific comparable sales the appraiser missed or identify specific errors in their analysis. Vague objections almost never succeed.

Why real estate appraisals matter more than you think

Here is the view most transaction advice skips entirely. An appraisal is not a hurdle you need to clear to get your loan. It is one of the most powerful pieces of evidence in your transaction, and most buyers and sellers leave that leverage on the table because they do not understand what the document actually contains.

Online estimates are useful for a rough sense of value. We use data tools ourselves, and we respect what algorithms can do. But an evidence-based appraisal process involves human judgment, physical inspection, and market expertise that no algorithm has replicated. An appraiser notices that the basement finish uses unpermitted work. They notice that the "four-bedroom" home has one room without a closet and a window that does not meet egress requirements. These are not things an online tool captures.

The second overlooked reality is that the appraisal report is a legal document tied directly to risk management. Lenders require it because they need independent proof of collateral value before committing hundreds of thousands of dollars. Courts use appraisals in estate settlements and divorce proceedings for the same reason. When you understand that, you start treating the appraisal as a tool that serves your interests, not just the lender's.

For sellers, a low appraisal is painful in the moment. But it is also an early warning signal. It tells you where objective market evidence places your property's value, regardless of what you hoped to get. The sellers who adapt quickly, either by renegotiating, making targeted improvements, or pricing more accurately on a relist, fare far better than those who fight the number without evidence. Understanding key factors in sale success means accepting that data beats emotion in real estate, every time.

Most buyers and sellers underestimate how much the appraisal shapes the deal. It is a contract protection mechanism, a negotiation anchor, and a due diligence document rolled into one. Treat it that way.

How HomeSavvy Colorado makes appraisal and valuation easier

If you want clarity on your home value or next steps, here's how HomeSavvy Colorado can support you. Understanding appraisals starts with knowing where your home stands before the formal process begins.

HomeSavvy Colorado gives you access to PropertyIQ, our AI-powered valuation tool, to get a data-backed estimate before you order a formal appraisal or list your home. It won't replace a licensed appraiser, but it gives you a realistic anchor point so you walk into negotiations informed. For sellers, our reduced listing fee model means you keep more of what the appraisal confirms your home is worth. For buyers, our commission rebate program gives you the financial cushion to handle appraisal gaps without derailing your purchase. Every tool we build is designed to put you in control of the data, not dependent on guesswork.

Frequently asked questions

Who pays for the real estate appraisal in Colorado?

Typically, the homebuyer pays for the appraisal as part of the loan process, though the cost can sometimes be negotiated into the sale contract as a seller concession.

How long does an appraisal take in Colorado?

Most appraisals are completed within three to seven business days of the inspection, though rural properties or high-demand periods can extend that timeline by several days.

Can I challenge an appraisal value I disagree with?

You can submit a formal reconsideration of value by providing comparable sales data or identifying specific factual errors in the report. Broad disagreements without supporting evidence are rarely successful.

Does a higher appraised value lower my property taxes in Colorado?

No. A lender-ordered appraisal has no effect on your property tax assessment, which is determined independently by your county assessor using different criteria and timelines.

Is an online home estimate the same as an appraisal?

No. An appraisal is a formal value opinion by a licensed appraiser built on evidence and reporting standards, while online estimates are algorithm-based approximations that cannot account for condition, permits, or property-specific factors.