Colorado property taxes are calculated by applying a state-set assessment rate to your property's market value, then multiplying that assessed value by local mill levies from school districts, counties, and special districts. For 2026, the residential assessment rate sits at 6.7% of actual market value, with a 10% reduction on the first $700,000 of value for primary residences. Understanding this formula is the foundation of every property tax bill in the state. This guide explains the full Colorado property tax process, from how your county assessor sets your value to how you can fight back if that number is wrong.

How do property taxes work in Colorado?

The Colorado property tax process starts with your county assessor determining your property's actual market value. That value is not the same as your purchase price or a Zillow estimate. County assessors use sales data from comparable properties within a defined lookback window to establish what your home would sell for on the open market.

Once market value is set, the state applies the assessment rate to produce your assessed value. For 2026, that rate is 6.7% for residential properties. A home with a market value of $600,000 carries an assessed value of roughly $40,200. That assessed value is the number your tax bill is actually based on, not the full market value.

Colorado also applies a primary residence reduction: 10% off the first $700,000 of actual value before the assessment rate is applied. On a $600,000 home, that means $60,000 is subtracted first, leaving $540,000 as the base for the 6.7% calculation. The result is an assessed value of about $36,180.

The two-year assessment cycle

County assessors reassess every two years. The 2025 reassessment set values that govern both 2025 and 2026 tax bills. The next reassessment happens in 2027. Between cycles, your assessed value changes only if there is a physical change to the property, such as an addition or demolition. This cycle matters because a hot real estate market can push your assessed value up significantly in a single reassessment year.

The repeal of the Gallagher Amendment in 2020 removed the constitutional cap that had kept residential assessment rates artificially low. Before repeal, rates were as low as 7.15% and declining. The legislature now sets rates directly, which is why the 2026 rate of 6.7% reflects a deliberate policy choice rather than an automatic formula. For a deeper look at how market value ties into appraisals, the Colorado real estate appraisal guide from Homesavvycolorado covers the relationship between appraised and assessed values in detail.

Pro Tip: Request your county assessor's comparable sales data as soon as you receive your Notice of Valuation. That data is the same evidence the assessor used to set your value, and reviewing it takes less than 30 minutes.

How are mill levies determined and what do they fund?

A mill levy is the tax rate applied to your assessed value. One mill equals $1 in tax for every $1,000 of assessed value. If your assessed value is $36,180 and your combined mill levy is 80 mills, your annual property tax bill is $2,894.

Mill levies across Colorado typically range from 60 to 120 mills depending on where you live. A homeowner in a rural county with minimal services pays far less than someone in a metro area with multiple overlapping taxing districts. That range translates to a difference of thousands of dollars per year on the same assessed value.

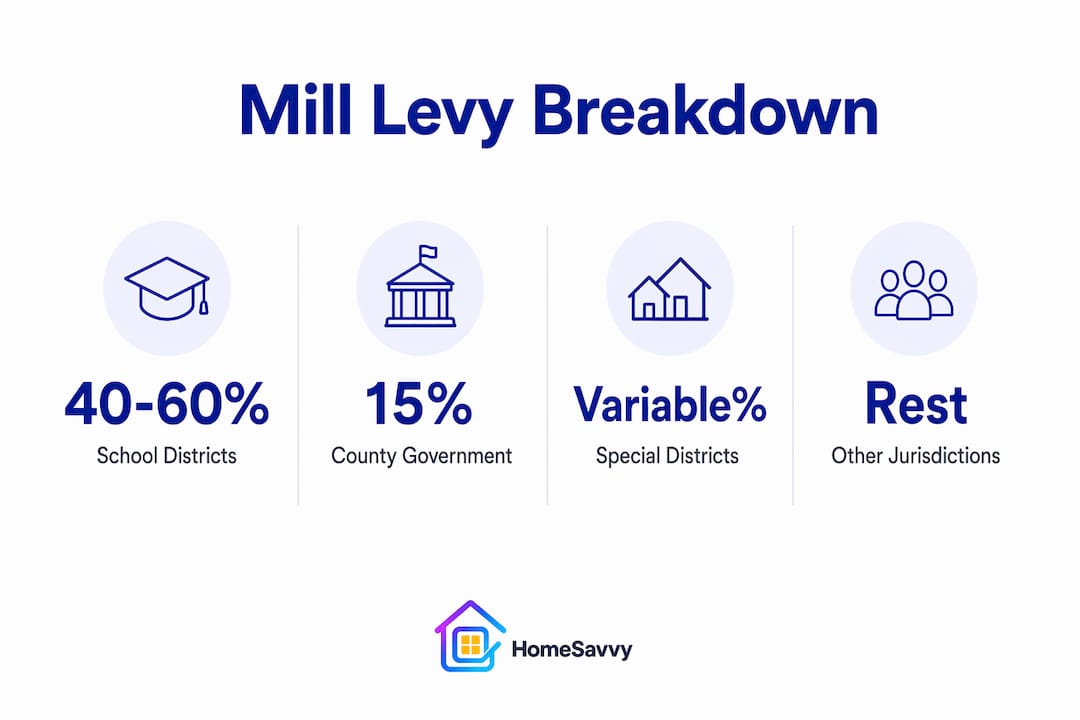

Your total mill levy is the sum of rates set by every taxing authority that has jurisdiction over your property. Those authorities include:

- School districts: The largest single component of most Colorado property tax bills, often accounting for 40% to 60% of the total mill levy.

- Counties: Fund roads, courts, public health, and county administration.

- Municipalities: Cities and towns add their own levy for local services like parks and police.

- Special districts: Metro districts, fire districts, water districts, and library districts each carry their own mill levy.

The breakdown matters more than most homeowners realize. Most property tax funding goes to school districts and special districts, not to city hall. A homeowner in Greenwood Village, for example, sees only a small fraction of their bill going to the city itself. The rest flows to Jefferson County R-1 or Cherry Creek School District and various special districts.

| Taxing authority | Typical share of mill levy |

|---|---|

| School districts | 40%–60% |

| County government | 15%–25% |

| Municipalities | 5%–15% |

| Special districts | 10%–25% |

Mill levies are set annually by each jurisdiction, and voter-approved measures can raise them. If your community passes a school bond or a fire district levy, your total mill levy increases the following year even if your assessed value stays flat.

What exemptions and credits are available to Colorado homeowners?

Colorado offers several property tax exemptions and credits that can significantly reduce what you owe. Many homeowners qualify and never apply.

The most valuable is the senior homestead exemption. It excludes 50% of the first $200,000 of actual residential value from property tax for homeowners aged 65 or older who have owned and occupied the property for at least 10 years. The state fully funds this exemption in 2026, meaning your county does not absorb the cost. You apply using form 15DPT-AR through your county assessor's office.

Other key exemptions and credits include:

- Disabled veteran exemption: Qualifying veterans with a service-connected disability of 100% receive a 50% exemption on the first $200,000 of actual value. Surviving spouses of qualifying veterans also qualify, with no minimum residency requirement.

- Primary residence reduction: The 10% reduction on the first $700,000 of actual value applies automatically to primary residences. You do not need to apply separately if your home is already classified as a primary residence.

- State income tax credit: Income tax credits up to $876 are available for low-income seniors and disabled residents. The income limit is approximately $19,700 for single filers. You claim this credit on your Colorado state income tax return.

- Property tax deferral: Colorado allows qualifying seniors and active military personnel to defer property tax payments. The deferred amount becomes a lien on the property, repaid when the home is sold or transferred.

- Senior work-off programs: Some counties and municipalities offer programs where seniors perform volunteer work in exchange for a reduction in their property tax bill. Boulder County and Jefferson County both run versions of this program.

Pro Tip: The senior homestead exemption is not automatic. You must apply by July 15 of the tax year. Missing that deadline means waiting another full year, which costs qualifying homeowners hundreds of dollars.

How can Colorado property owners appeal their assessment?

Filing a protest is one of the most underused tools available to Colorado homeowners. A timely protest filed by June 1 with your county assessor can save hundreds to thousands of dollars over the two-year assessment cycle. The process is more straightforward than most people expect.

Here is how the appeal process works step by step:

- Review your Notice of Valuation. County assessors mail this notice in May. It states your property's assessed market value for the current cycle. Check the value against recent sales of comparable homes in your neighborhood.

- File an informal protest with your county assessor by June 1. Most major counties, including Denver, Jefferson, and Arapahoe, accept online filings. Submit comparable sales data showing homes similar to yours that sold for less than your assessed value.

- Receive the assessor's decision. The assessor reviews your evidence and responds by the last working day in June. If the assessor agrees, your value is reduced. If not, you move to the next step.

- Appeal to the County Board of Equalization (CBOE). You have until July 15 to file with the CBOE. This is a formal hearing where you present your evidence to a panel. No attorney is required.

- Escalate to the State Board of Assessment Appeals or district court. If the CBOE rules against you, further appeal options exist at the state level, though these are rarely necessary for residential properties.

Comparable sales data is the strongest evidence you can bring. Focus on homes that sold within the assessor's lookback window, are similar in size and condition, and are located in your immediate neighborhood. Professional representation is not required. Missing the June 1 deadline forfeits your right to challenge the assessed value for the entire two-year cycle, so calendar that date the moment your Notice of Valuation arrives.

Pro Tip: Pull your own comparable sales from public county records or ask a real estate agent for a quick market analysis. Three to five solid comps showing lower values are usually enough to support a successful informal protest.

What buyers and sellers should know about Colorado property taxes

Property taxes are a direct component of monthly homeownership cost, and buyers who ignore them during the purchase process often face surprises after closing. A $700,000 home in a high-mill-levy district can carry a tax bill $3,000 to $5,000 higher per year than an identical home in a lower-levy area. That difference affects affordability calculations and mortgage qualification.

Key considerations for buyers and sellers include:

- Review the tax history before making an offer. County assessor websites publish current and prior year tax bills. Comparing the seller's actual tax payments to your projected costs after reassessment gives you a realistic picture of carrying costs.

- Factor in the next reassessment. If you buy in 2026, the 2027 reassessment will set a new value based on current market conditions. In a rising market, your tax bill could increase substantially in year two of ownership.

- Negotiate tax prorations at closing. Colorado property tax bills are paid in arrears, meaning 2025 taxes are paid in 2026. At closing, sellers typically credit buyers for the portion of the current year's taxes that accrued during the seller's ownership. Verify this calculation carefully.

- Sellers should check for pending appeals. If you filed a protest and the outcome is still pending at the time of sale, disclose this to the buyer and clarify who receives any refund.

- Use data tools to estimate post-purchase taxes. The Colorado property evaluation checklist from Homesavvycolorado walks buyers through how to assess tax exposure before committing to a purchase.

Understanding how property tax policy affects buying is not optional for serious buyers in Colorado's competitive market. The difference between two otherwise identical homes in neighboring districts can be thousands of dollars annually.

Key takeaways

Colorado property taxes are determined by three factors: your property's assessed market value, the state-set assessment rate of 6.7%, and local mill levies that range from 60 to 120 mills depending on your jurisdiction.

| Point | Details |

|---|---|

| Assessment rate for 2026 | Residential properties are assessed at 6.7% of market value, with a 10% reduction on the first $700,000 for primary residences. |

| Mill levy range | Combined mill levies run from 60 to 120 mills; school districts receive the largest share of collected taxes. |

| Senior homestead exemption | Homeowners aged 65+ with 10 years of occupancy can exempt 50% of the first $200,000 of actual value. |

| Protest deadline | File your informal protest with the county assessor by June 1 or forfeit appeal rights for the full two-year cycle. |

| Tax paid in arrears | Colorado property taxes are billed in January for the prior year, so buyers and sellers must account for prorations at closing. |

What I've learned after watching homeowners leave money on the table

Most Colorado homeowners treat their property tax bill like a utility payment. It arrives, they pay it, and they move on. That approach costs real money.

The single most common mistake I see is failing to review the Notice of Valuation when it arrives in May. That document is not just a formality. It is the county's opening position in a negotiation you are allowed to enter. In a market where assessed values jumped significantly during the 2025 reassessment cycle, thousands of homeowners are paying taxes on values that do not reflect what their home would actually sell for today.

The protest process is genuinely accessible. You do not need a tax attorney or a property tax consultant. You need three to five comparable sales and 45 minutes to file online. I have seen homeowners in Jefferson County and Arapahoe County reduce their assessed values by $50,000 to $80,000 through informal protests alone, which translates to $300 to $600 in annual savings and double that over the two-year cycle.

The senior homestead exemption is another area where eligible homeowners consistently miss out. The application is simple, the savings are real, and the state fully funds it in 2026. If you or a family member qualifies, there is no reason to delay.

One more thing worth saying plainly: mill levies vary so much across Colorado that the same house in two different zip codes can carry tax bills that differ by $4,000 or more annually. Local knowledge is not a nice-to-have when you are buying property. It is a financial necessity.

— Rishi

See your estimated property taxes before you commit

Understanding your property tax exposure before you buy or sell is exactly what Homesavvycolorado built its tools to support.

The PropertyIQ AI Home Valuation tool gives Colorado homeowners and buyers a detailed estimate of market value and projected tax assessments, pulling from real-time data across Colorado counties. If you are buying, it helps you model total ownership costs before you make an offer. If you are selling, it shows you how your assessed value compares to current market conditions. Homesavvycolorado also offers buyers significant commission rebates and sellers a 1% listing fee, so the savings extend well beyond your tax bill.

FAQ

What is the residential assessment rate in Colorado for 2026?

The 2026 residential assessment rate is 6.7% of a property's actual market value. Primary residences also receive a 10% reduction on the first $700,000 of actual value before the rate is applied.

How do I calculate my Colorado property tax bill?

Subtract 10% from the first $700,000 of your home's market value, apply the 6.7% assessment rate to get your assessed value, then multiply by your local mill levy divided by 1,000. Mill levies typically range from 60 to 120 mills across Colorado counties.

Who qualifies for the senior homestead exemption in Colorado?

Homeowners aged 65 or older who have owned and occupied their primary residence for at least 10 consecutive years qualify. The exemption removes 50% of the first $200,000 of actual value from taxation and must be applied for by July 15.

When is the deadline to protest my property tax assessment?

The informal protest deadline with your county assessor is June 1. Missing this date forfeits your right to challenge the assessed value for the entire two-year assessment cycle.

Are Colorado property taxes paid in advance or in arrears?

Colorado property taxes are paid in arrears. Your 2025 tax bill arrives in January 2026 and is due in two installments: February 28 and June 15. Buyers and sellers account for this through tax prorations at closing.